The best (and worst) ways to redeem points for online shopping

Signing up for credit cards through partner links earns us a commission. Terms apply to the offers listed on this page. Here’s our full advertising policy: How we make money.

Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

If you’re like most of us in the miles and points hobby, your belt is distressed and fraying in December 2020. Our pockets are overloaded with credit cards extra-heavy from the hundreds of thousands of points we’ve been accruing while we’re busy not traveling.

If you’ve been doing your best to stock up on miles and points by opening a travel credit card as they come out with ludicrous intro offers (bookmark our Bonus Tracker to stay informed of the latest unprecedented bonuses), you’re likely set to easily travel for free for the next year or two.

If, however, you’ve got no desire to head back out into the world anytime soon, you may be wondering what your points can do for a homebody. You may even be scheming to save big on holiday shopping with them.

I’ll give you the five most common ways to use your points for online shopping — and tell you whether or not it’s a good deal.

How to use points for online shopping

Shop on Amazon (Bad deal, with one exception)

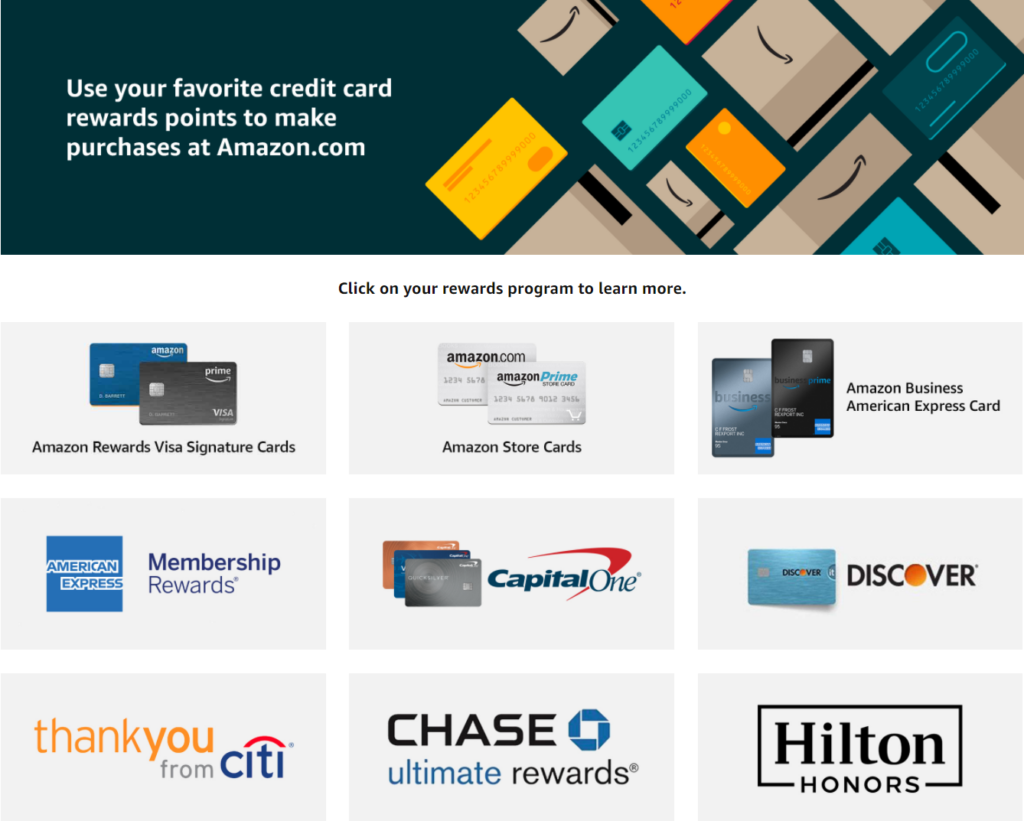

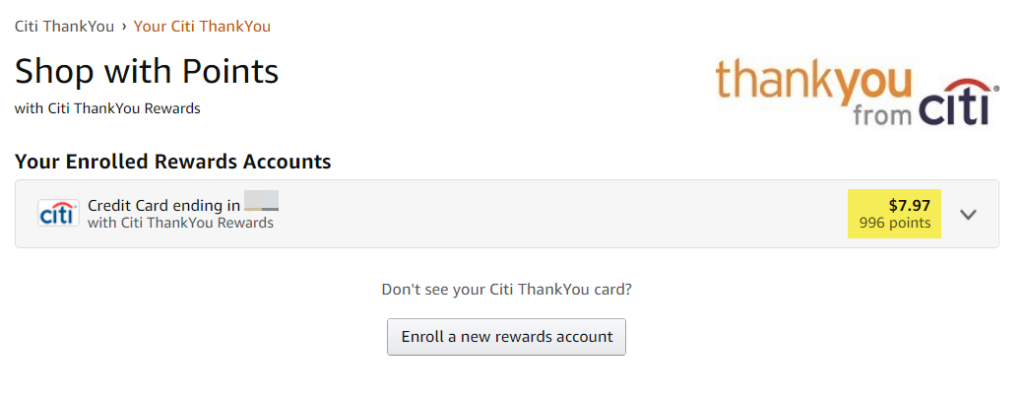

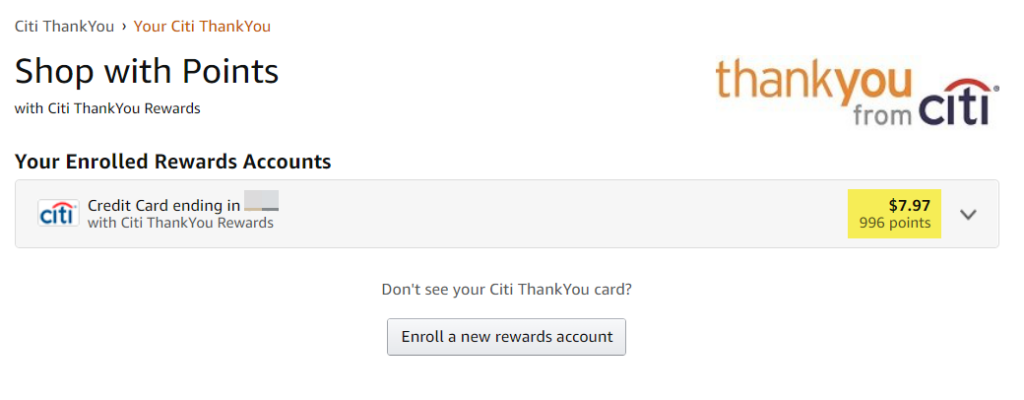

When you follow this link, you can add lots of different points currencies to your Amazon payment methods.

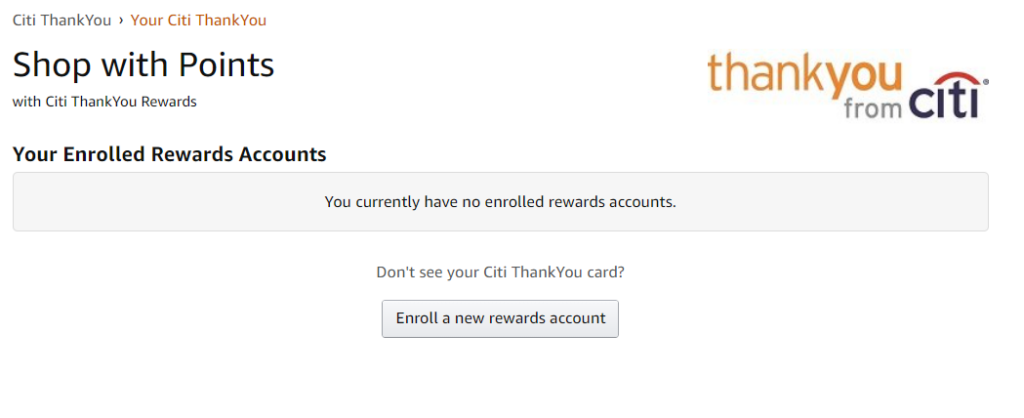

Click on a tile, and you’ll have the opportunity to link your rewards account to Amazon by entering the info of the credit card that earns those specific points. I’ll enter my Citi Premier® Card info to link my Citi ThankYou points.

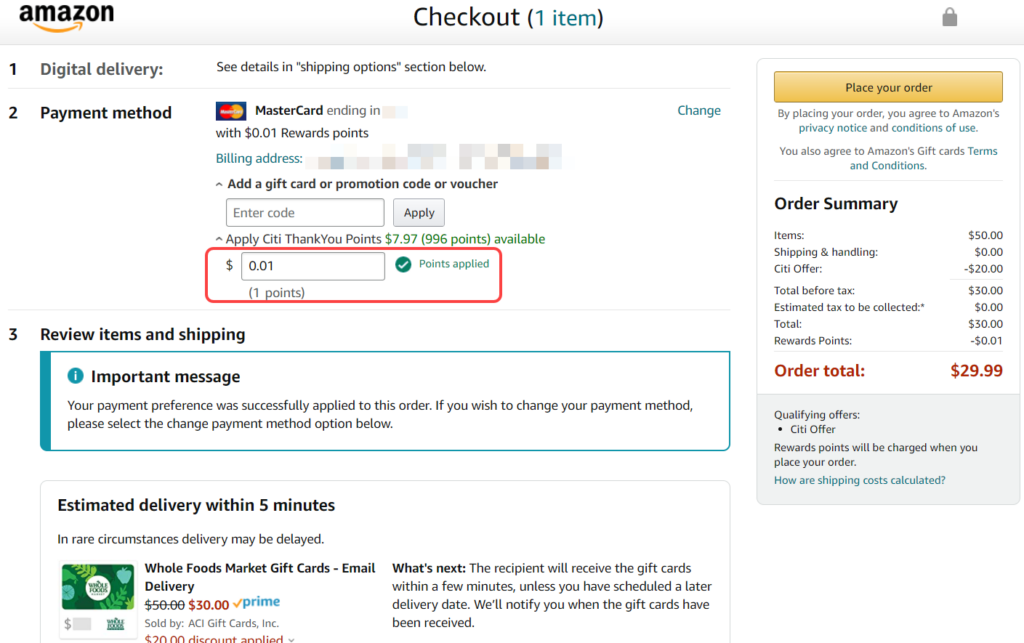

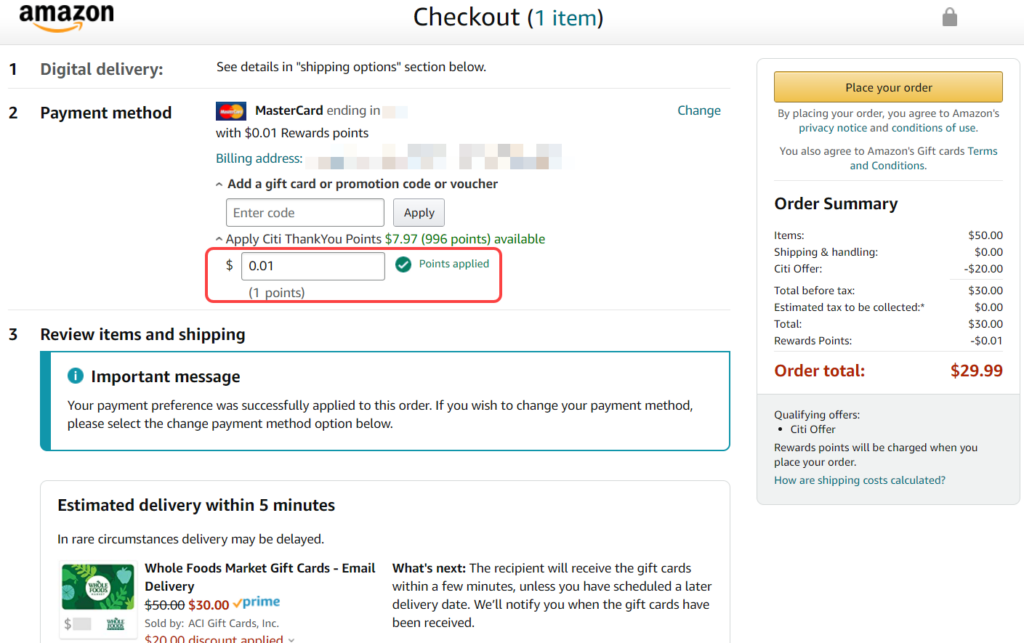

Once added, you can see how many points are available from that card. I’ve only got 996 ThankYou points at the moment, which are worth $7.97 each. That amounts to 0.8 cents each. A truly offensive deal.

Here’s the value you will receive from the major points programs for Amazon’s shop with points program:

- American Express – 0.7 cents (88% less than our Amex points valuation)

- Chase – 0.8 cents (72% less than our Chase points valuation)

- Citi – 0.8 cents (72% less than our Citi points valuation)

- Capital One – 0.8 cents (66% less than our Capital One miles valuation)

Yikes. You’ll get far more value when redeeming your points for travel, or even straight cash back, compared to non-travel items. There’s one exception which I’ll mention below where redeeming points towards Amazon purchases does make sense.

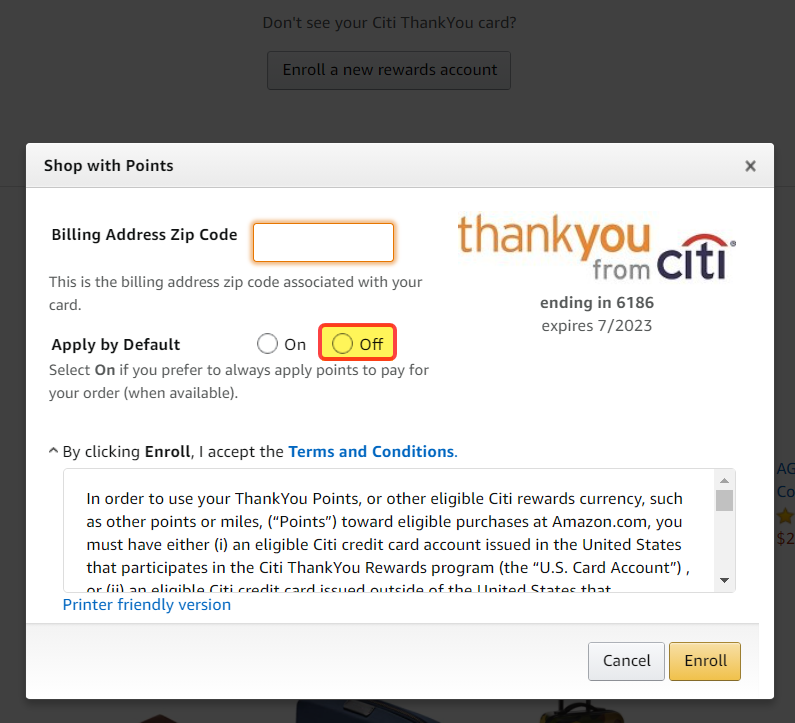

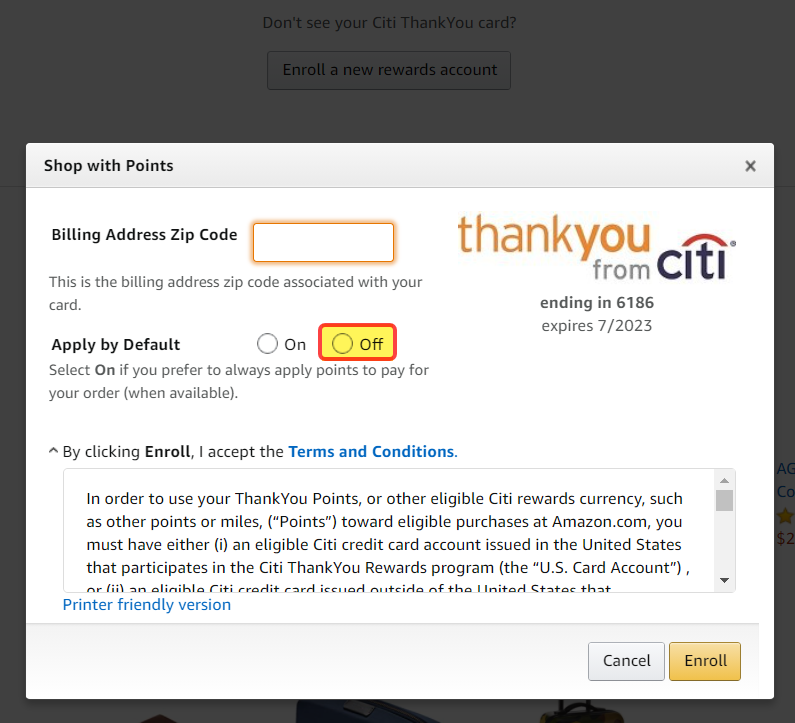

On that note, when linking your account, be sure to select “Off” when asked if you want your default payment option to be points. This way you don’t accidentally blow a ton of points next time you’re speeding through Amazon checkout.

Look for “single-point promotions” (AMAZING deal)

There are surprisingly frequent promotions that allow you to redeem your credit card points for big discounts while online shopping. Amazon is the biggest participant in these deals.

Here’s how they work: Once your rewards accounts are linked to Amazon, you need to make your payment with a mix of cash and points — doesn’t matter how many of each. And because redeeming points with Amazon provides poor value, it’s the best strategy to use only one point and use cash for the rest.

For example, Amazon recently published a $20 discount off $50+ orders when using at least one Citi ThankYou point at checkout. I used it to buy a $50 Whole Foods gift card for $30.

This is hands-down the single best value you will ever get for points. By using a single point, I saved $20.

Amex offers these deals most frequently, sometimes allowing you to save $60 on an Amazon order by using just one Amex point.

Redeem points for gift cards (BAD deal — usually)

You can redeem points for gift cards, often at a rate of 1 cent per point or worse. Here are the standard rates for each program:

- Chase – 1 cent each (52% less than our Chase points valuation)

- Citi – 1 cent each (52% less than our Citi ThankYou points valuation)

- American Express – Usually around 0.7 cents (57% less than our Amex points valuation)

- Capital One – 1 cent each (18% less than our Capital One miles valuation)

You can study our points valuations for more explanation.

As you can deduce from the value we place on the above rewards, going the gift card route is usually a bad deal. I say usually because there are occasionally some generous gift card discounts that boost the value of your points — sometimes up to 50% — for those particular redemptions.

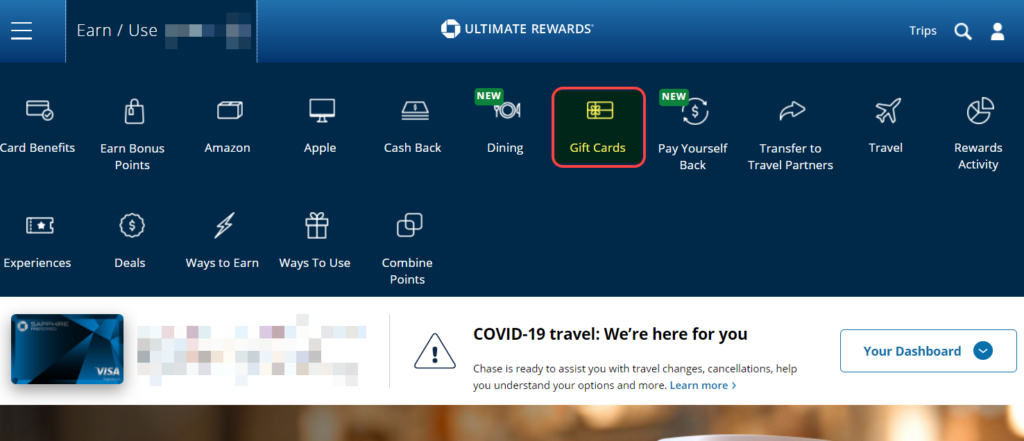

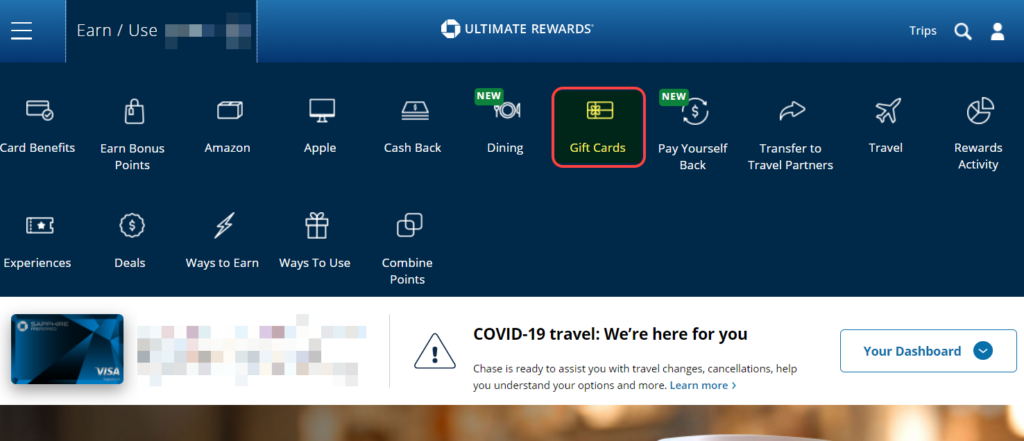

For example, on the Chase Travel Portal right now, you can find plenty of discounted gift cards. Just sign-on through this link. Find and click on the Gift Cards option from the drop-down menu.

You can redeem your points for merchants like Home Depot, Apple, Gamestop, Cheesecake Factory, Bed Bath & Beyond, and tons more for 10% off.

Just cash out (Better deal than most)

If you’re set on shopping online with your points, cashing them out can be a better deal than redeeming for gift cards or using them at checkout for your Amazon cart.

Here are each rewards programs’ cash out rates

- Chase – 1 cent per point (or up to 1.5 cents per point — I’ll explain below)

- Citi – 0.5 cents per point (1 cent per point if you have the Citi Prestige® Card)

- Amex – 0.6 cents per point (1.25 cents per point if you have the American Express Platinum Charles Schwab Card)

- Capital One – 0.5 cents per mile

As you can see from the parenthetical tips, it’s possible to get a value greater than or equal to gift cards with nearly every rewards program. And that’s hard cash that you can spend on whatever you want — you’re not tied to gift card merchants. Plus, when you use your card to pay for your online shopping, you’ll earn points, too! Not so if you redeem points for gift cards.

For example — perhaps you recently opened the Ink Business Cash® Credit Card and earned its monster $7,500 bonus cash back (or 75,000 points) after spending $7,500 in the first three months of account opening. You could redeem that gift card for $750 in Staples gift cards towards a laptop. Or, you could:

- Spend $750 to buy the computer

- Earn 5 points per dollar at Staples, totaling $37.50 in cash

- Cash out your 75,000 points for $750

- Be $37.50 richer than if you had used your points for gift cards

I want to point something out about Chase points. Through Sept. 30, 2021, you can use a feature called Chase Pay Yourself Back, which allows you to redeem points for a statement credit to offset spending on groceries, home improvement stores, and dining. Here’s the rate at which you can redeem with the following cards:

- Chase Sapphire Preferred® Card – 1.25 cents each

- Chase Sapphire Reserve® – 1.5 cents each

This requires a bit of “proxy” thinking, but you can effectively cash out your points at up to 1.5 cents each with this method. For example, if you want a $300 curved monitor, simply use 20,000 Chase points (with the Sapphire Reserve) to reimburse $300 in groceries this month. You will then have a spare $300 to spend on your curved monitor.

Chase’s Pay Yourself Back feature will get you the most “cash” for your points, and is strongly worth considering if you have no travel plans in 2021 or beyond.

Random promotions

There are out-of-left-field promotions that may drop in your lap from time to time. They still aren’t the best around (no consistent option will be better than using your points the way God intended — for travel), but if you’re sitting on a mound of points and you’ve got no upcoming plans, they could be for you.

We’ve recently seen Chase lower the number of points needed when redeeming for Apple products by 50%. We’ve even seen Amex reduce their redemption prices for merchandise by 30%. If you subscribe to our newsletter, we’ll let you know when a worthwhile deal pops up so you can cash in.

Which cards earn these points?

To earn Chase points, our favorites are:

- Chase Sapphire Preferred® Card

- Chase Sapphire Reserve®

- Ink Business Cash® Credit Card

- Ink Business Unlimited® Credit Card

- Ink Business Preferred® Credit Card

- Chase Freedom Flex℠

To earn Citi ThankYou points, open:

- Citi Rewards+® Card

- Citi Premier® Card

- Citi® Double Cash Card

- Citi Prestige® Card

The information for the Citi Double Cash Card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

To earn Amex points, your best bets are:

- The Platinum Card® from American Express

- American Express® Gold Card

- American Express® Green Card

- American Express® Business Gold Card

- The Business Platinum Card® from American Express

To earn Capital One miles, open:

- Capital One Venture Rewards Credit Card

- Capital One Spark Miles for Business

- Capital One VentureOne Rewards Credit Card

- Capital One Spark Miles Select for Business

The information for the Amex Green, Citi Prestige, Capital One Spark Miles and Capital One Spark Miles Select has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

Bottom line

If you can help it, always redeem your miles and points for travel. You will save often double and triple the value you’d receive cashing them in for online shopping.

If, however, you’re so flush with points that you don’t mind getting a cringy value for them, happy shopping! Free stuff is free stuff. Just note that if you make a habit of redemptions like this, it’s possible you’ll be better served from a cash back card like the no annual fee Citi® Double Cash Card instead of a travel credit card card.

Let me know if you’ve redeemed your points for online shopping — and if you’ve got any tricks up your sleeve! And subscribe to our newsletter for more points how-tos like this delivered to your inbox once per day.

Editorial Note: We're the Million Mile Secrets team. And we're proud of our content, opinions and analysis, and of our reader's comments. These haven’t been reviewed, approved or endorsed by any of the airlines, hotels, or credit card issuers which we often write about. And that’s just how we like it! :)

Join the Discussion!